India’s payments regulator is set to decide as early as Monday whether to curb the dominance of Walmart’s PhonePe and Google in the nation’s fast-growing mobile payments market, a move that could reshape how its billion-plus population moves money.

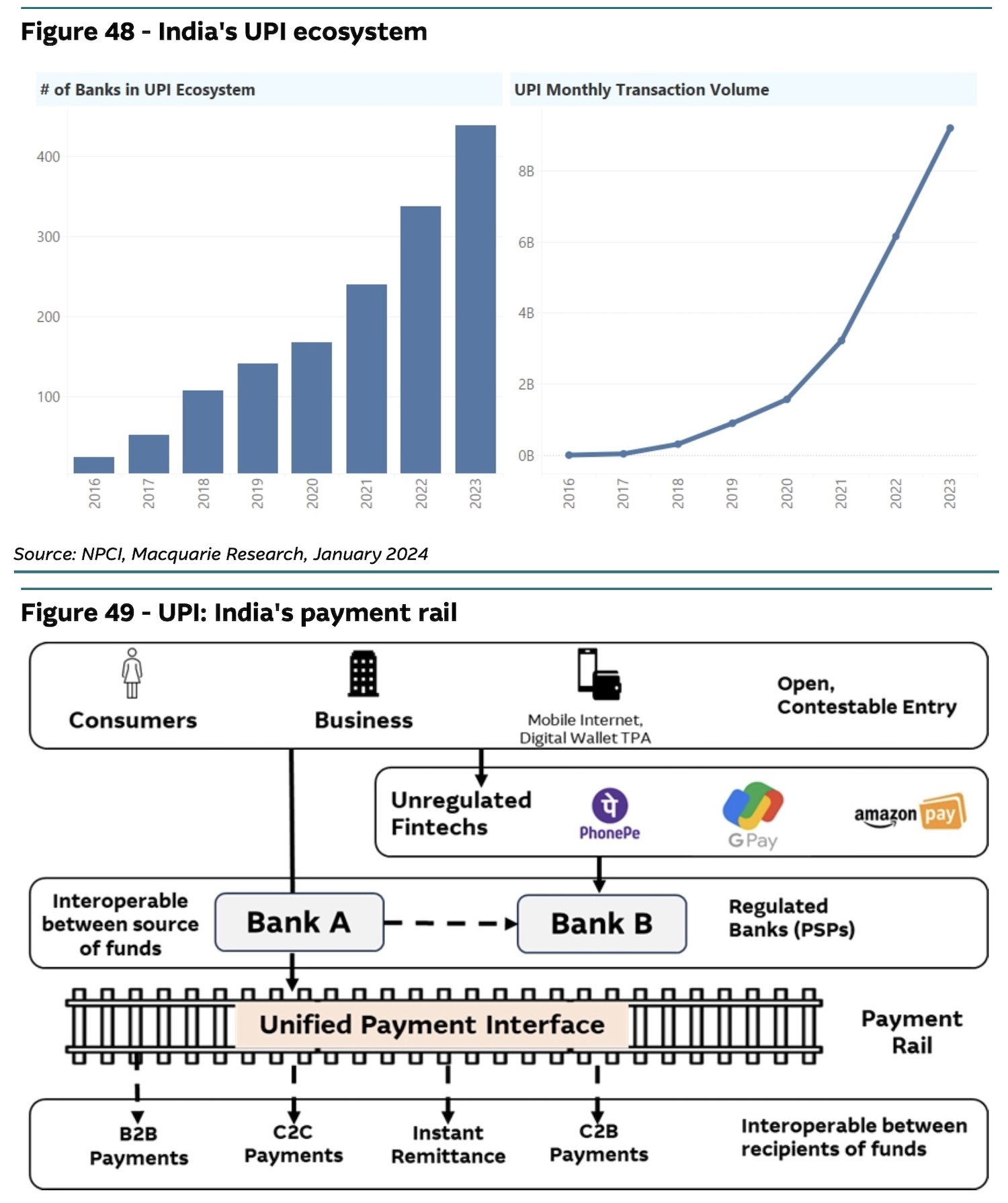

The decision centers on UPI, or Unified Payments Interface, a network backed by more than 50 retail banks that has changed how Indians pay for everything from groceries to taxi rides. The platform processes over 13 billion transactions monthly, making it one of the world’s largest digital payment networks. It’s also, by far, the most popular way Indians transact online.

At issue is whether the National Payments Corporation of India, which reports to India’s central bank, will enforce a rule limiting companies to handling no more than 30% of all UPI transactions.

The rule, first proposed in 2020, would particularly affect Walmart-owned PhonePe, which handles 47.8% of all UPI payments, and Google Pay, which processes 37.1%.

The uncertainty has thrown a wrench into PhonePe’s plans to go public. The startup, valued at $12 billion and backed by Walmart, would be one of India’s most prominent technology IPOs. PhonePe’s co-founder and chief executive, Sameer Nigam, said in August that the startup cannot go public “if there is uncertainty on the regulatory side.”

“If you are buying a share at Rs 100 and you price it assuming we have 48-49% market share, then there is an uncertainty about whether it will come down to 30% and by when,” said Nigam (pictured above) at a fintech conference. “We are requesting them [the regulator], if they can find another way to at least solve whatever their concerns are or tell us what the list of concerns is.”

The issue also impacts the growth potential of numerous fintech startups that are attempting to make deeper inroads in digital payments. If the regulator imposes restrictions on PhonePe and Google Pay’s ability to onboard new users or puts a check on how many transactions they process, many other startups stand to gain grounds.

The regulator is inclined to delay enforcing the cap again or may increase the limit to more than 40%, people briefed on the situation told TechCrunch. The agency has already pushed back the deadline several times, from January 2021 to 2023, and then to 2025, as it struggled with implementation. It has held talks with many stakeholders as recently as last week over the decision.

Enforcing a limitation on the market share will impact the consumer experience, some of the people said.

The situation highlights India’s efforts to balance technological innovation with market competition. UPI has been a cornerstone of Prime Minister Narendra Modi’s push to digitize India’s economy and reduce its reliance on cash. The system allows instant transfers between bank accounts using simple identifiers like phone numbers, making it more accessible than traditional banking services.

A market share cap would mark one of India’s most significant interventions in its technology sector, which has attracted massive investments from global companies like Walmart, Google, and Meta. These companies view India, with its young, increasingly digital population, as a crucial growth market.