Paytm has agreed to sell its stake in Japanese payments firm PayPay to SoftBank for $279.2 million, as the Indian firm sheds non-core assets following a bruising regulatory clampdown earlier this year.

PayPay, controlled by SoftBank and Yahoo Japan parent Z Holdings, is a leading payments app in Japan.

The stake sale will boost Paytm’s cash reserves to $1.46 billion as it attempts to recover market share in India’s fiercely competitive payments market. The company’s banking affiliate was severely restricted by regulators in January, leading to an exodus of customers to rival services.

Shares in Paytm have nearly tripled since June after India’s payments regulator allowed it to resume adding customers to its flagship UPI service. The company reported its first quarterly profit in September, though this was largely due to proceeds from asset sales rather than operational improvements.

“We are grateful to Masayoshi-san and the PayPay team for giving us the opportunity to together create a mobile payment revolution in Japan,” Paytm said in a statement. “We remain fully committed and will continue to support PayPay’s product and technology innovations in future. We are working on introducing new AI-powered features to accelerate PayPay’s vision in Japan.”

Saturday’s deal marks the end of Paytm’s relationship with SoftBank, which divested its remaining shares in June after being an early backer through its Vision Fund.

Paytm, a leading Indian financial services firm, has received regulatory approval to resume adding new UPI payments users, following an eight-month restriction on many of its operations.

UPI, which processes over 15 billion monthly transactions, dominates India’s online payments. Walmart-owned PhonePe and Google Pay process about 87% of UPI transactions, whereas Paytm’s market share has shrunk from 13% to 8% after this year’s central bank restrictions.

The Reserve Bank of India ordered Paytm to cease many of the businesses at its affiliate payments bank early this year over repeated violation of rules. NPCI, the regulatory body that oversees UPI, approved Paytm’s application on Tuesday.

Analysts at Bernstein and Goldman Sachs said the approval is a “significant” development that will help revive Paytm’s transacting user growth. Paytm’s monthly transacting users has fallen to 68 million as of last month from 100 million in December.

Paytm on Tuesday reported revenue of $197.4 million in the quarter ending September, up from $178.6 million in the previous quarter but down 34% year-on-year from $299.5 million. Profit in the quarter climbed to $110 million after factoring in a one-time gain of $160 million from the sale of entertainment ticketing biz to Zomato.

Zepto is in advanced stages of talks to raise $100 million in new investment, its third in the last six months, as the leading Indian quick commerce startup looks to rope in more domestic investors, sources familiar with the talks told TechCrunch.

The Mumbai-headquartered startup, which delivers grocery items and office stationery to customers’ doorsteps in 10 minutes in multiple Indian cities, is raising the new investment from Indian family offices and high net worth individuals.

Motilal Oswal, the asset management giant that earlier invested $40 million in Zepto, is running the mandate for the new funding deliberation, the sources said, requesting anonymity as the matter is private. The financial services firm has already received commitments for more than half of the allocation, according to another source familiar with the situation.

The new investment values Zepto at a $5 billion post-money valuation, the same value at which it recently closed a $340 million financing round in August. Zepto has raised more than $1 billion in the last six months and all of it remains in its bank.

Zepto is planning to go public next year and the new fundraise is aimed at expanding the base of domestic investors on its cap table. Zepto counts Avra, Lightspeed, Nexus, StepStone Group, YC Continuity, Glade Brook and Contrary among its backers.

Even as quick commerce startups are retreating, consolidating or shutting down in many parts of the world, the model is showing encouraging signs in India. Quick commerce startups are on track to do a sale of more than $6 billion this year, according to TechCrunch’s analysis.

In response to the fast rise of quick commerce, which is increasingly shaping the consumer behavior in India, many e-commerce incumbents — including Flipkart, Myntra and Nykaa have been forced to scramble ways to lower the time they take to deliver items to their customers.

Shares of Dmart, which runs one of the largest brick-and-mortar retail chains in India, fell this week after the firm confirmed that it was losing some business to quick commerce startups.

“We believe Quick Commerce players are expanding cities, categories, SKUs, AOVs and discounts, and creating parallel commerce for convenience-seeking customers,” analysts at Morgan Stanley wrote in a note this week.

Zepto – which competes with Zomato-owned BlinkIt, Prosus-backed Swiggy’s Instamart, and Tata’s BigBasket – has grown its annualized net runrate considerably in recent months, according to sources and an internal document reviewed by TechCrunch.

Star Health and Allied Insurance, one of the largest health insurance firms in India, has confirmed it was the target of a “malicious cyberattack,” some two weeks after cybercriminals claimed to post customers’ health records and other sensitive data online.

The Chennai-headquartered insurance giant told TechCrunch in a statement Wednesday that the cyberattack resulted in “unauthorized and illegal access to certain data,” though it stated its operations remained unaffected and services continued.

“A thorough and rigorous forensic investigation, led by independent cybersecurity experts, is underway, and we are working closely with government and regulatory authorities at every stage of this investigation, including by duly reporting the incident to the insurance and cybersecurity regulatory authorities apart from filing a criminal complaint,” the company said in its statement.

When asked by TechCrunch, Star Health would not say if the data breach included customers’ data.

Last month, a hacker group created chatbots on Telegram that leaked the alleged personal data belonging to 31 million Star Health policyholders and over 5.8 million insurance claims. The data included full names, phone numbers, and home addresses, as well as medical reports and insurance claims of individuals. The hackers also shared copies of customer ID cards and individuals’ tax details.

Shortly after the hackers’ Telegram bots came to light, Star Health filed a legal complaint with the Madras High Court against Telegram for hosting the chatbots. The insurer also named Cloudflare in its lawsuit for its role in hosting the hacker group’s websites on its service.

India’s CERT-In told TechCrunch earlier that it was “already in process of taking appropriate action with the concerned authority.”

Details of the breach, and how the hackers obtained potentially millions of customers’ data, remain unclear.

The hackers’ website, used to publicize the Telegram bots sharing the allegedly stolen person data, includes a video allegedly showing screenshots and conversations between Star Health CISO Amarjeet Khanuja and the hacker group. TechCrunch is not linking to the site as it contains personally identifiable information.

The role of the company’s CISO in the cyberattack, if at all, is not yet known.

“We also want to categorically mention that our CISO has been duly co-operating in the investigation, and we have not arrived at any finding of wrongdoing by him till date. We request that his privacy be respected as we know that the threat actor is trying to create panic,” the insurer said Wednesday.

TechCrunch asked specific questions, including whether the insurer can confirm who accessed the data, whether it was an insider or a malicious intruder, and if it knows and can confirm what has been accessed or taken already. The insurer would not say.

Star Health, which provides health, personal accident, and overseas and travel insurance, has a network of more than 14,000 hospitals and over 850 branch offices across India. Star Health says on its website that it has provided health insurance coverage to 170 million individuals.

India’s commerce minister Piyush Goyal on Wednesday expressed concern over the rapid growth of e-commerce in the country, warning of potential disruption to small retailers.

Speaking at the launch of a report on the impact of e-commerce on employment and consumer welfare in India, Goyal said the projected dominance of online marketplaces in the coming decade was worrying rather than praiseworthy.

“Are we going to cause huge, social disruption with this massive growth of e-commerce? I don’t see it as a matter of pride that half our market may become part of the e-commerce network 10 years from now; it is a matter of concern,” Goyal said, adding that the e-commerce market was doubling in size every four years.

India’s $1.1 trillion retail market saw e-commerce sales of less than $80 billion last year, according to HSBC. The e-commerce sector’s growth rate stands at 11%-12% annually. Quick commerce startups, which promise deliveries in 10 minutes or less, are experiencing rapid expansion. BlinkIt (owned by Zomato), Swiggy Instamart (backed by SoftBank) and Zepto (backed by Lightspeed) are projected to collectively achieve over $4.5 billion in sales this year, a year-on-year growth rate exceeding 100%, according to a TechCrunch analysis.

E-commerce firms are going after the high-margin products that brick-and-mortar stores sell, something that small retailers rely on for their survival, Goyal said. “How many mobile stores do you see now at the corner? How many were there 10 years ago? Where are those stores?”

He criticized the pricing strategies of major e-commerce firms, questioning whether their reported losses indicated predatory pricing.

A major investment by Amazon in India is celebrated, he said, but people are forgetting “the underline story — that this billion dollars is not coming for any great service or investment to support the Indian economy.”

“They made a billion dollar loss in their balance sheet that year, they had to fill in that loss… If you make Rs 6,000 crore ($715M) loss a year doesn’t it sound like predatory pricing to you? They are after all an e-commerce platform, they are not allowed to do B2C, legally…However, reality is all of you buy on these platforms, how are they doing it? Should it not be a matter of concern for us?”

Indian law requires Amazon, Flipkart and other e-commerce players to operate as pure marketplaces in the country. The e-commerce firms cannot own the inventory they sell — a lesson they have learned the hard way.

“I am not wishing away e-commerce,” Goyal said Wednesday. “I don’t deny that e-commerce has a role, but we have to think very cautiously what that role is.”

Uber is rolling out concurrent rides in India, a feature that allows users to book up to three trips for any of their contacts, TechCrunch has exclusively learned and confirmed with the company.

The concurrent rides feature is the latest example of Uber developing products that will capture more customers, including those who don’t have the app or even a smartphone. In India, Uber even allows concurrent ride users to pay drivers directly with cash or via the app.

Uber quietly launched the concurrent rides last year in several global markets, including the United States. An Uber spokesperson confirmed the new feature is now available in India and will be rolled out in the country in a phased manner. The spokesperson would not confirm the exact details of the cities in which it is currently available.

“As we understand that one may need to book a ride for their loved one at the same time as they are in an Uber — we launched concurrent rides late last year globally. It allows riders to book and track up to three concurrent rides,” an Uber spokesperson said in a statement shared with TechCrunch.

Once a user books a ride for a guest, those trip details can be shared over WhatsApp or a text message. The message contains the driver’s full name, cab model and registration number, Uber’s contact number to reach the driver, a link to track the ride, and a four-digit PIN to start the ride. This eliminates the need for guests to use the Uber app.

The new feature could help Uber expand its market reach. Before the update, Uber was allowing only one ride booking at a time, and users had to request another vehicle after their current trip ends. It also pushes Uber ahead of rivals that were already offering customers to the ability to book concurrent rides.

Uber’s Indian competitor, Ola, which counts Softbank, Warburg Pincus and DST Global among its key investors, has allowed two concurrent rides for some time. However, the experience offered by Ola is limited as it does not allow users to make two bookings simultaneously using a single online payment method. You need to either choose two different online payment methods or pay for your concurrent rides via cash.

Zapp Electric Vehicles wants to turn its London-based electric two-wheeler brand into a global EV company. And India will be one of its launchpads, TechCrunch has exclusively learned.

The company will launch its first product — an urban electric two-wheeler called the i300 — in the UK as early as next month, followed by Thailand. The company is now adding India into the mix, a massive market that will provide a true test to its international global expansion strategy, Zapp founder and CEO Swin Chatsuwan told TechCrunch in an interview.

The Nasdaq-listed company advanced its plans for India after Chatsuwan noted the country’s potential. The world’s most populous country not only witnesses millions of two-wheeler sales annually, it’s also the second-biggest two-wheeler manufacturer worldwide after China.

“We thought India would be phase two for us when we did our research a few years ago, but we made a decision earlier this year that it can’t wait,” Chatsuwan said.

Zapp has named Indian electric two-wheeler maker Bounce Electric 1 as its contract manufacturer to produce and sell the i300 locally in the country. After completing the homologation process, sales are expected to begin in 2025. The British company aims to have a minimum capacity of 5,000 units per year in India as part of its broader global goal of 25,000 units by 2026.

Of the 17 million two-wheelers sold in India last year, Chatsuwan told TechCrunch that 2.8 million were high-speed vehicles, and 36% of those high-speed vehicles were heavy-weight cruiser motorcycles from the Chennai-based brand Royal Enfield. Zapp wants to duplicate Royal Enfield’s success with its step-through model, which was unveiled first in 2018.

“We’re not trying to conquer the world. We’re not trying to take half Royal Enfield’s market share and sell 500,000 bikes in India. We’re not. We would see that our quality and performance peer is BMW, particularly their CE 02 and CE 04 step-through electric scooters,” the executive told TechCrunch.

The India launch of Zapp’s i300 will help the company expand its total addressable market (TAM) of 60 million units annually by 25%. By adding India to the map, the TAM of its first phase of market debut has reached 30 million annually, the company said.

The early launch in India will help Zapp understand the “breadth, depth and quality” of the country’s supply chain, Chatsuwan stated. This may help export vehicles from India to global markets over time.

Unlike electric two-wheelers by key Indian manufacturers Ola Electric, TVS Motor and Ather Energy that sell between $1,000 and $1,800, Zapp’s i300 will be a pricey option. The two-wheeler will debut in Europe with a base price of $7,590, excluding taxes.

The India pricing is yet to be decided, though Chatsuwan said it wouldn’t be “more than a million rupees, but I doubt it will be lower than 500,000 rupees.”

The i300 is hitting the streets soon

Zapp unveiled the i300 as its first two-wheeler in 2018. The vehicle comes with an aerospace-grade alloy load-bearing exoskeleton and a chrome-moly steel underbone design. It also carries an air-cooled electric motor with a peak power of 14kW and packs two portable batteries, each with 720Wh capacity.

The company started taking pre-orders for the i300 soon after its unveiling, charging a reservation fee of 100 euros. It promised to begin deliveries in the fourth quarter of 2019. However, the COVID-19 pandemic halted production and deliveries.

Image Credits: Zapp EV

Nonetheless, Zapp is set to start delivering the i300 in the U.K. in the next few weeks. It also plans to begin selling in Thailand this year through a facility in Bangkok.

Zapp set to become ‘complete motorcycle company’

“We’re not a one-hit wonder. We want to show the world that we’re a complete motorcycle company, but let’s begin with executing the first product first,” Chatsuwan told TechCrunch when asked whether Zapp looks to expand its product lineup.

The company also plans to stack up the i300 with “loads of” personalization options and accessories. It already offers the two-wheeler in four distinct versions and lets consumers customize its color and wheel design based on their preference and add accessories, including a hidden storage and fast charger.

Zapp plans to expand its market by entering Spain, Italy, Vietnam and Indonesia in phase two and expand to countries in the Middle East and South America over time.

“We want to be the 21st-century version of Triumph and Royal Enfield and Norton,” Chatsuwan said.

Avendus, the top investment bank for venture deals in India, confirmed on Wednesday it is looking to raise up to $350 million for its new private equity fund.

The new fund, called Future Leaders Fund III, will enable the Mumbai-headquartered firm to write larger checks and maintain a meaningful position in the startups it backs, said its managing partner Ritesh Chandra in an interview with TechCrunch. TechCrunch reported in early April that Avendus was putting together a plan to raise a new fund.

A regular fixture in most growth-stage deals in India, Avendus has established itself as the largest venture advisor for startups in the country. It provided services in over 30 deals last year, including merger and acquisition transactions, according to Venture Intelligence, a private market insight platform. The growing size of its private equity unit underscores the firm’s ambitions to extend its tentacles even more deeply into the ecosystem and see more upside from the winnings.

The firm’s rise to prominence was aided by the fact that many of its well-established global rivals, such as Goldman Sachs, Morgan Stanley, and JP Morgan, initially paid less attention to the Indian market, allowing Avendus to gain a foothold and build relationships with the country’s burgeoning tech entrepreneurs.

Those relationships are also helping the firm’s private equity unit to gain access to some of the high-profile deals. Aside from lead backer SoftBank, the financial services startups Juspay and Zeta have allowed only Avendus on their cap tables, for instance. “These are businesses that came out of our relationships and networks,” said Chandra.

Avendus’ private equity unit, whose portfolio includes Delhivery, Lenskart, Licious, VerSe Innovation, Xpressbees, and the National Stock Exchange, has also earned a reputation for delivering large exits to its backers in a timely manner. LensKart and the National Stock Exchange, for instance, both delivered four times the money Avendus invested within four years of investments.

“Our fund’s lifecycle is five to six years. A problem with the Indian startup ecosystem is that investors have poured a lot of capital [into it] but don’t see returns for a long period of time. We are focused on how do we get our money back,” Chandra said.

Despite the growing trend of tech startups in India going public, a phenomenon that was uncommon just four years ago, investors cannot solely rely on IPOs for returns. According to Chandra, Avendus has established relationships that enable the company to exit its positions by selling stakes to late-stage investors, such as sovereign investors, providing an alternative avenue for generating returns apart from IPOs.

Some Indian government websites have allowed scammers to plant advertisements capable of redirecting visitors to online betting platforms.

TechCrunch discovered around four dozen “gov.in” website links associated with Indian states, including Bihar, Goa, Karnataka, Kerala, Mizoram and Telangana that were redirecting to online betting platforms. Some of those websites belong to state police and property tax departments in the respective states. The scammy links were indexed by search engines, including Google, making the ads easy to find online.

The redirecting websites, touted as “Asia’s most popular” online betting platform and “the number one online cricket betting app in India,” claim to allow betting on games, including cricket tournaments such as the Indian Premier League.

It’s not clear how the scammers planted the ads on Indian government pages or for how long the links were redirecting to the online betting platforms.

Image credits: Google / TechCrunch

After spotting the issue earlier this week, TechCrunch alerted India’s Computer Emergency Response Team, known as CERT-In, to the lapse and provided a few affected state government website links for reference.

Shortly after, the Indian cyber agency acknowledged the receipt of the email, and on Thursday CERT-In confirmed it escalated the matter.

“We have taken up with the concerned authority for appropriate action,” the agency said in an email response. It is not clear if the flaw allowing the backdoor access to state government websites has been fixed.

Last June, TechCrunch reported that scammers had published ads for hacking services on U.S. government websites by way of a security flaw in the government’s web content management system software. Some of those ads appeared to be available online for years.

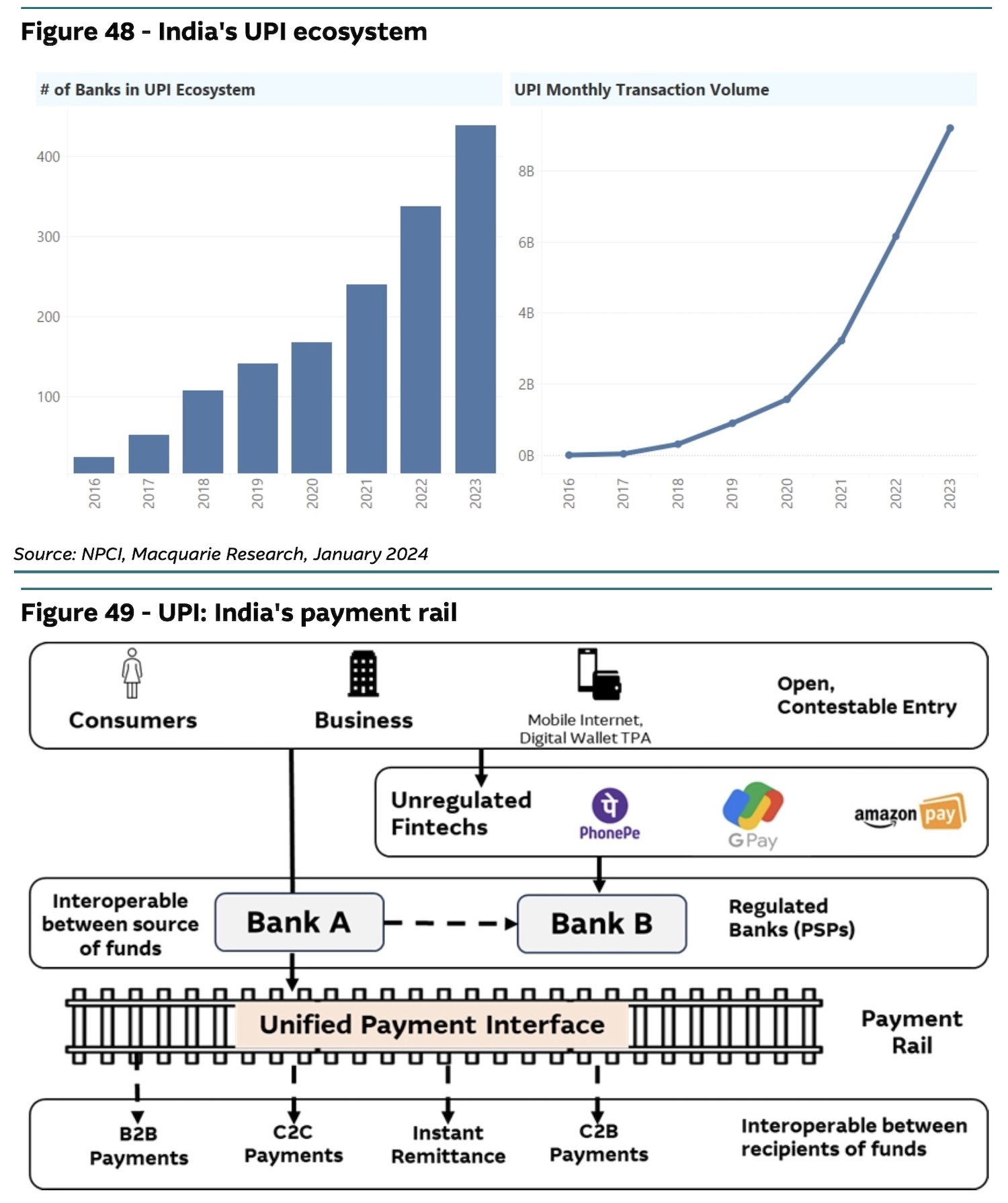

The National Payments Corporation of India (NPCI), the governing body overseeing the country’s widely used Unified Payments Interface (UPI) mobile payment system, is set to engage with various fintech startups this month to develop a strategy to address the growing market dominance of PhonePe and Google Pay in the UPI ecosystem.

NPCI executives plan to meet with representatives from CRED, Flipkart, Fampay and Amazon among other players to discuss their key initiatives aimed at boosting UPI transactions on their respective apps and to understand the assistance they require, people familiar with the matter told TechCrunch.

UPI, built by a coalition of Indian banks, has become the most popular way Indians transact online, processing over 10 billion transactions monthly.

The new meetings are part of an increasing effort to address concerns raised by lawmakers and industry players regarding the market share concentration of Google Pay and PhonePe, which together account for nearly 86% of UPI transactions by volume, up from 82.5% at the end of December. Walmart owns more than three-fourths of PhonePe.

Paytm, the third-largest UPI player, has seen its market share decline to 9.1% by the end of March, down from 13% at the end of 2023, following a clampdown by the Reserve Bank of India (RBI).

An overview of India’s UPI ecosystem. (Image: Macquarie)

The conversation follows the central bank expressing “displeasure” to the NPCI over the growing duopoly in the payments space, a person familiar with the matter said. An NPCI spokesperson declined to comment.

In February, a parliamentary panel in India urged the government to support the growth of domestic fintech players that can offer alternatives to the Walmart-backed PhonePe and Google Pay apps.

The NPCI has long advocated for limiting the market share of individual companies participating in the UPI ecosystem to 30%. However, it has extended the deadline for firms to comply with this directive to the end of December 2024. The organization faces a unique challenge in enforcing this directive: It believes that it currently lacks a technical mechanism to do so, TechCrunch previously reported.

The RBI is also weighing an incentive plan to create a more favorable competitive field for emerging UPI players, another person familiar with the matter said. Indian daily Economic Times separately reported Wednesday that the NPCI is encouraging fintech companies to offer incentives to their users, promoting the use of their respective apps for making UPI transactions.